Most people don’t feel like they have personal finance figured out. Money comes in, money goes out, and the end of the month often feels like a bit of a mystery.

The truth is, managing money doesn’t have to be complicated. You don’t need advanced strategies or a high income to get started. You just need a few simple habits that give you clarity and control.

Let’s break it down.

Budgeting: understanding where your money goes

A budget is simply a way of giving your money direction instead of guessing where it went.

Start with the basics: your monthly income and your expenses. Once you lay everything out—rent, groceries, bills, subscriptions—you usually get a clearer picture pretty quickly.

Most people don’t actually realize how much small, repeated spending adds up until they look at it in one place.

You don’t need anything fancy to do this. A notes app or a simple spreadsheet is enough.

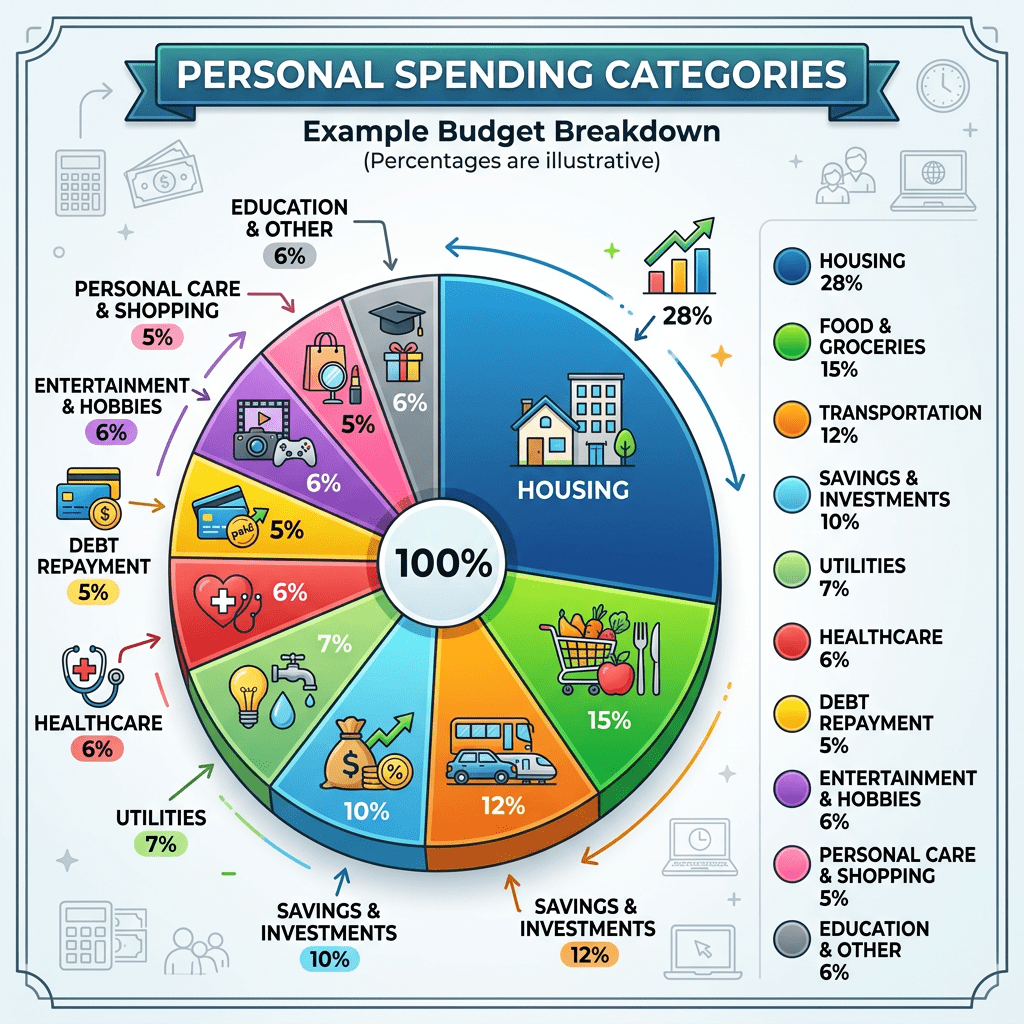

From there, it helps to group spending into a few categories:

- Essentials (rent, utilities, food, transport)

- Lifestyle spending (eating out, entertainment, subscriptions)

- Savings and debt payments

A common structure people use is the 50/30/20 rule, where income is split between needs, wants, and savings. It’s not a strict formula you have to follow—it’s just a reference point.

The goal of budgeting isn’t restriction. It’s awareness. Once you understand your spending, you can adjust it intentionally.

Saving: building a financial buffer

Saving money is often treated as something you do “if there’s anything left over.” In reality, that approach rarely works.

A better method is to save first, even if the amount is small.

Start with something realistic—$10, $25, maybe $50 per paycheck. The exact number isn’t as important as building consistency.

If possible, automate it so the money moves into savings without you needing to think about it. Over time, this removes the temptation to spend it elsewhere.

A good starting goal is building a small emergency fund. Even a few hundred dollars can make unexpected expenses far less stressful. From there, you can gradually build toward covering a month or more of expenses.

Saving isn’t about perfection. It’s about creating a cushion that gives you options.

Debt: getting organized and making progress

Debt becomes more manageable once you actually lay it all out clearly.

Start by listing everything you owe—credit cards, loans, balances, interest rates, and minimum payments. Many people avoid this step, but clarity is what makes a plan possible.

Once you see the full picture, there are two common ways to approach repayment:

One option is to focus on the smallest balance first. This can build momentum because you get quick wins early on.

The other is to focus on the highest interest debt first, which reduces the total amount you pay over time.

Neither approach is wrong. The most effective strategy is the one you can stay consistent with.

What matters most is making progress beyond minimum payments. Even small extra payments can reduce debt faster than most people expect.

Bringing it all together

If you’re starting from scratch, the process doesn’t need to be overwhelming.

A simple starting point looks like this:

- Track your income and spending

- Set a basic, realistic budget

- Start saving something consistently

- Create a plan to reduce debt

That alone puts you ahead of a lot of people financially.

Final thought

Personal finance isn’t really about being perfect with money. It’s about being intentional with it.

Once you start paying attention to where your money is going, you gain the ability to actually change it. And that’s where real progress starts—not with complexity, but with awareness and consistency.

Leave a comment